For months already, high-yield savings accounts have been paying their best rates in 20 years. Yet they keep raising the ceiling on how much you can earn. Today’s unveiling of a new national leader raises the bar to a top rate of 5.35% APY—with another nine options paying 5.25% APY or better.

The rate crown for high-yield savings accounts now belongs to BrioDirect, an online bank operated by the brick-and-mortar Webster Bank. While you have to make an initial deposit of at least $5,000 to open the account, after that you only need to keep $25 in the account to earn their record rate.

Plenty of Options for Earning a Historically High Rate

Every day, we publish our ranking of the best high-yield savings accounts, offered by banks and credit unions that accept customers nationwide. So even if you don’t like the requirements of the very top rate in our rankings, you have more than a dozen additional options that are still paying one of the country’s most elite savings account rates.

| Current Savings Account Rate Leaders – Nationally Available Accounts | |||

|---|---|---|---|

| Rate | Minimum Initial Deposit | Minimum Ongoing Balance | |

| BrioDirect | 5.35% APY | $5,000 | $25 |

| BluPeak Credit Union | 5.33% APY | $25 | Any amount |

| TotalDirectBank | 5.26% APY | $25,000 | $2,500 |

| Milli | 5.25% APY | $0 | Any amount |

| Newtek Bank | 5.25% APY | $0 | Any amount |

| UFB Direct | 5.25% APY | $0 | Any amount |

| Valley Direct | 5.25% APY | $1 | Any amount |

| Evergreen Bank Group | 5.25% APY | $100 | Any amount |

| Vio Bank | 5.25% APY | $100 | Any amount |

High-Yield Savings Accounts Are a Very Smart Move

With savings and money market accounts paying their highest rates in about 20 years, it’s a smart move to keep some of your money in one of these high-yield accounts. While your checking account is probably paying no interest, and even a savings account at your primary bank may be paying close to zero, a high-yield savings account instead offers the chance to earn almost 12 times the national average rate of 0.45% APY.1

Not used to holding money somewhere other than your primary bank? Don’t fret that it will be too inconvenient, or that it will be less safe. In fact, all of the banks in our ranking of the best savings accounts are federally insured by the Federal Deposit Insurance Corp. (FDIC). That means up to $250,000 of your deposits—per person and per institution—are covered in the unlikely event that the bank fails. And that’s true whether the FDIC bank is a brick-and-mortar institution or an online-only bank.

Credit unions are less common contenders for the best high-yield savings accounts. But still, they offer the same protection as FDIC banks, insured instead by the National Credit Union Administration (NCUA). Just like FDIC banks, deposits held at NCUA credit unions are protected up to $250,000 per person and per institution.

As for convenience, online banking makes transfers between institutions extremely easy these days. And though the transfer process can take one to three days, you can plan for this by not moving every penny of your savings to the new account. Just keep some portion in reserve where you have your checking account, in case you need an immediate transfer.

Put Some Savings in a CD to Earn Even More

Want to give your interest earnings a turbo boost? An additional smart move is to transfer a portion of your savings into a top-paying certificate of deposit (CD). Though you won’t have access to funds put in a CD for months or years, depending on the term you choose, the rates available from the best nationwide CDs are even higher than the best high-yield savings account. The current CD rate leader is paying 5.80% APY. Remember: What you lock in with a CD is the rate you keep for the full length of the certificate.

Just keep in mind that cashing out your CD before its maturity date will incur an early withdrawal penalty, so it’s best to think carefully about how much you can lock away and for how long.

| Account Type | Today’s Top Nationally Available Rate | National Average Across All FDIC Banks1Federal Deposit Insurance Corporation. “National Rates and Rate Caps.” |

|---|---|---|

| High-yield savings account | 5.35% APY | 0.45% APY |

| Money market account | 5.25% APY | 0.65% APY |

| 3-month CD | 5.66% APY | 1.37% APY |

| 6-month CD | 5.76% APY | 1.36% APY |

| 1-year CD | 5.80% APY | 1.76% APY |

| 18-month CD | 5.80% APY | Not tracked |

| 2-year CD | 5.50% APY | 1.51% APY |

| 3-year CD | 5.23% APY | 1.38% APY |

| 4-year CD | 5.00% APY | 1.31% APY |

| 5-year CD | 5.00% APY | 1.38% APY |

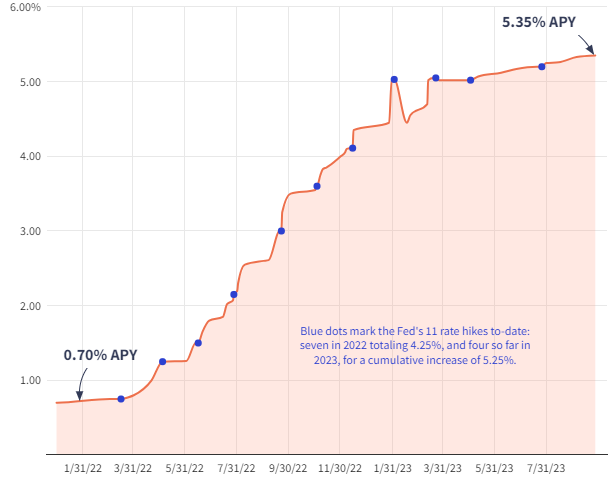

Will Savings Account Rates Go Higher This Year?

Savings rates are directly influenced by what the Federal Reserve does with the federal funds rate. And since March 2022, the Fed has been moving this benchmark rate aggressively higher, implementing seven bold and rapid rate hikes in 2022, plus four more increases in 2023 so far. This has brought the central bank’s total increase to 5.25% so far.2

Federal Reserve. “Open Market Operations.”

The Fed’s fast-and-furious rate-hike campaign has pushed banks and credit unions to raise savings, money market, and CD rates to record levels. In fact, today’s top savings account rate of 5.35% APY is likely the highest we’ve seen since 2001, since that’s the last time the fed funds rate has been this high.2

The Fed won’t make another rate announcement until Nov. 1, and at this time, the Fed is keeping its options open. In fact, Fed members have publicly made it clear that another rate increase is still on the table if inflation doesn’t come down far enough and reliably enough.

Forecasting Fed moves is an uncertain exercise, especially when making predictions months down the road. But it’s reasonable to expect that savings rates will likely hold somewhat stable for the time being—with the possibility of inching a little higher if the Fed opts to raise rates another time.

Rate Collection Methodology Disclosure

Every business day, Investopedia tracks the rates of almost 100 banks and credit unions that offer savings accounts to customers nationwide, using that data to determine daily rankings of the top-paying accounts. To qualify for our lists, the institution must be federally insured (FDIC for banks, NCUA for credit unions), and the savings account’s minimum initial deposit must not exceed $25,000.

Banks must be available in at least 40 states. And while some credit unions require you to donate to a specific charity or association to become a member if you don’t meet other eligibility criteria (e.g., you don’t live in a certain area or work in a certain kind of job), we exclude credit unions whose donation requirement is $40 or more.